Australian house prices hit record high for fifth consecutive month

CoreLogic data shows prices rose 0.6% in March while separate index from PropTrack produces similar results.

National home values set a record high for a fifth consecutive month in March as a resilient economy and the swelling population pointed to further increases to come.

The home value index compiled by data group CoreLogic showed prices rose 0.6% last month, matching February’s increase. Median home prices were $772,730, rebounding just over one-tenth since its recent nadir in January 2023.

A separate index run by PropTrack produced similar results. National home prices were 0.34% higher in March to be up 6.79% from a year earlier, also a fresh peak.

“Demand has been quite resilient in the face of very high interest rates, high cost-of-living pressures, affordability challenges and very low [consumer] sentiment,” said Tim Lawless, CoreLogic’s research director.

With population growing by some measures at the fastest pace since the 1950s and new housing approvals sinking, “there’s an imbalance here between demand and supply that doesn’t look like it’s going to be fixed anytime soon”, he said

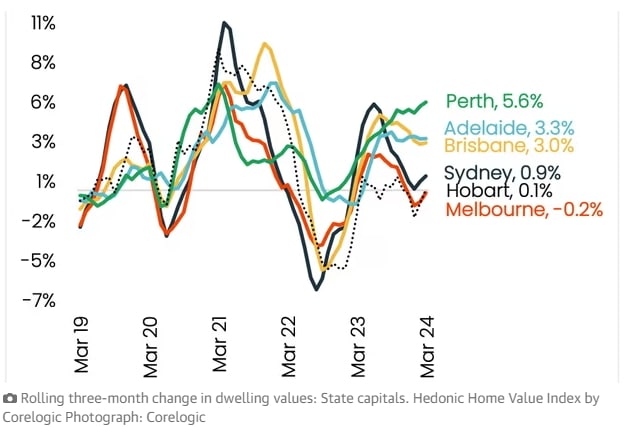

Among the state capitals, home values rose in all cities in the March quarter except for Melbourne, CoreLogic said. Sydney remained the most expensive city while Perth, Adelaide and Brisbane are all at record levels after steep rises in the past year.

The Reserve Bank’s 13 interest rate rises since May 2022 have sent mortgage payments soaring, particularly for households who took out loans when the cash rate hit a record low of 0.1% during the pandemic.

So far, though, mortgage arrears have only ticked up modestly and remain below pre-Covid levels. Should unemployment remain near half-century lows and interest rates start to retreat later this year, home price increases look like increasing at least as fast as the current pace.

Sales volumes, for instance, were 9.5% from subdued levels of the March quarter of 2023. Turnover was about 3.7% higher than the past decade’s average for this time of year, CoreLogic said.

One sign of strains on affordability, though, was a shift in demand towards the cheaper end of the market. Prices for the lowest quartile of home rose 3.1% in the January-March period, compared with a 0.7% increase for the most expensive 25% of the market.

Pricier homes tend to rise in value first, coming out of dip. Since the September quarter, though, the lower quartile has been rising faster than the upper end of the sector, Lawless said.

“Serviceability assessments [of loans] are becoming harder given high cost of living pressures and higher interest rates as well,” he said. “If you’re on a median household income, it’s pretty hard to buy the medium price dwelling in this sort of market.”

That tilt towards rising prices for lower-cost home may also reflect the desperation of some renters to shield themselves from an “unrelenting level of rental growth” and a low level of vacancies in many parts of the country, Lawless said.

“We have seen first homebuyers over-represented in the market,” he said. “They’re about 28% of owner-occupier demand compared to a long-run average of about 24%.”

CoreLogic’s national rental index was up 2.8% in the March quarter, the fastest pace in almost two years.

Unit rents were rising at 2.9% in the March quarter, slightly higher than the 2.7% pace for house rentals.

Gross rental yields are on the rise too, a prospect that may lure more investors back into property. Melbourne, for instance, saw its average rental yield – the annualised rent on a on a property divided by its value – reach 3.57% in March, or the city’s highest since March 2015, according to CoreLogic.

The property sector, though, is not without its headwinds. Affordability issues remain a drag that may get heavier should unemployment pick up faster than economists currently expect, Lawless said.

The RBA will be also less inclined to cut interest rates if its see a re-ignition of consumption because homeowners feel wealthier as their assets rise in value.

“The last thing regulators would want to see is another house price boom,” Lawless said. “It’ll be interesting to see what the policy response could be if housing prices start to take off more substantially because there are only a few levers that can be pulled.”